The Fed, Payrolls, Regional Banks and Q1 Earnings in 400 words

What can we glean from Fed hikes, regional bank woes, and Q1 earnings.

What did we learn this week? (04/28/2023)-Sometimes History Doesn't Even Rhyme

There is a mountain of evidence suggesting a recession is near, but this cycle has been characterized by some supportive dynamics that are unique from previous cycles.

Tim Pierotti’s Quarter 2 Insights

In this video, Tim discusses what to expect during quarter 2 2023, and the factors stressing today’s economy.

What did we learn this week? (04/20/2023/)-Humility

What Wall Street sell-side analysts expected to happen over the past 2 years and what happened are dramatically different. When will negative earnings revisions matter?

Liquidity and Wages

I thought I would share the two charts that I think are most important to what is going on with equity markets and with the Fed. The top chart shows the correlation of the S&P and the Fed balance sheet. As I wrote last week, the markets love a bailout. The economy has clearly slowed through the first quarter. Credit availability is sharply contracting and earnings estimates for the S&P in Q1 are expected to decline by 7% y/y. So why are risk assets rallying? I think this chart tells you all you need to know. I would also add that when so many macro investors (Hedge Funds) are positioned short, that creates a bid under the market as those entities have to cover their short positions to manage risk as the market rises.

What Did We Learn This Week? (04/11/2023) - Foreboding Credit Data

Tim explores the question: Is bad economic data good for the stock market?

Quick Thoughts on OPEC, ISM’s, GDP and Liquidity in 400 Words

Goldman’s Head of Commodity Research said yesterday, “OPEC’s pricing power is the highest it’s ever been.” The Saudi’s want oil in the $90 to $100 range. They see demand weakening globally, so they cut production. Importantly, they aren’t worried about losing global market share because US shale production is no longer the threat it had been due to shale’s declining productivity and declining rate of resource investment.

The China demand recovery hasn’t materialized like the oil bulls hoped. Makes sense given the property sector is already overbuilt and and the Chinese export economy isn’t getting any help from slackening European and the US demand.

Don’t Borrow Trouble

We have plenty of things to worry about in the US economy with the cost of debt going up and its availability going down, but European bank CoCo’s probably isn’t one of them.

Ryan Fabian joins WealthVest Team to Expand Wholesaling Support

WealthVest, a financial services marketing and wholesaling firm, announced that Ryan Fabian, a financial planning professional, has joined their nationwide team as a Regional Consultant.

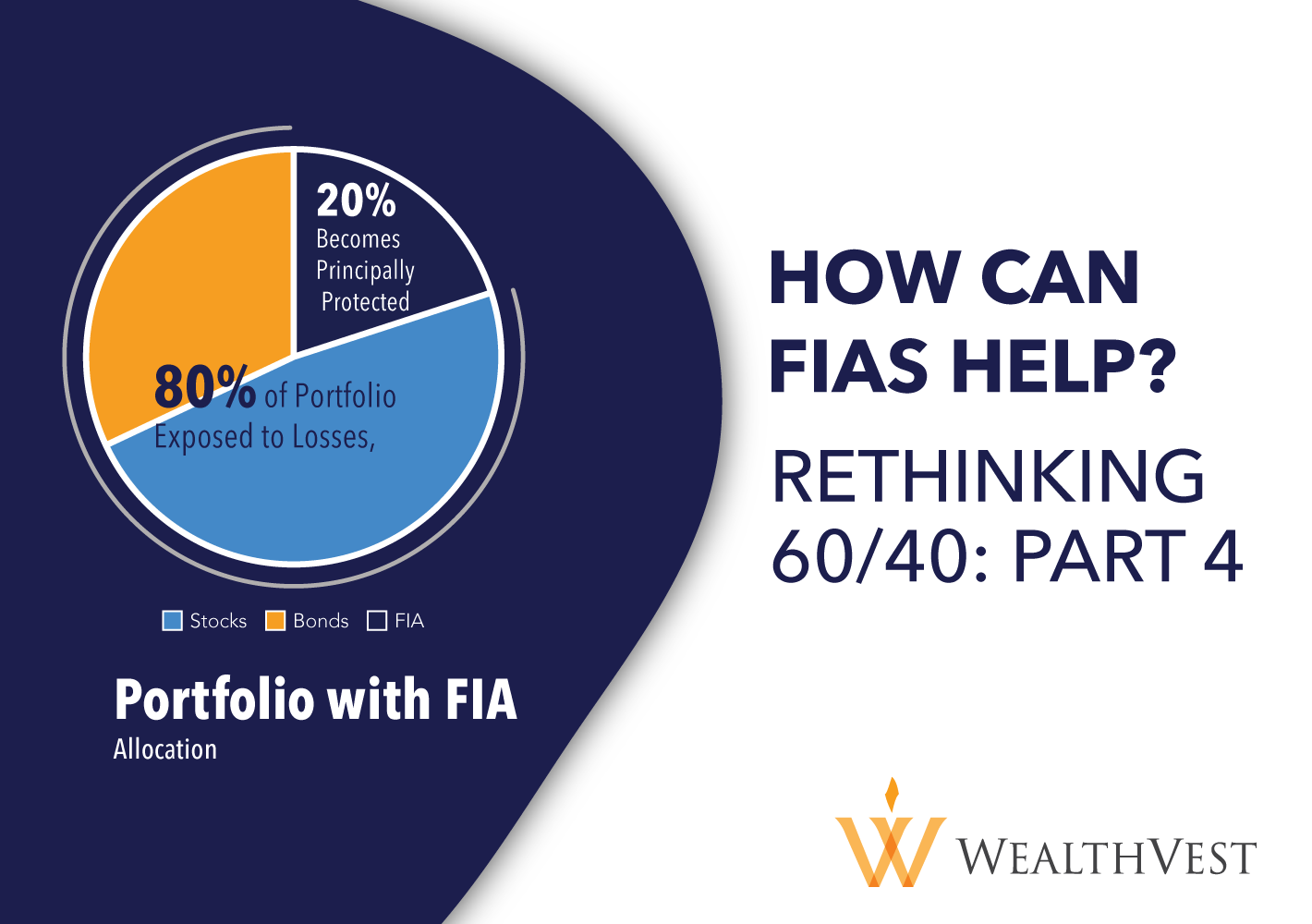

Rethinking 60/40 Part 4: How Fixed Index Annuities Can Help

WealthVest believes that there is a natural fit for FIAs within optimized portfolios A fixed index annuity is a type of fixed annuity that offers a rate of return based on market performance. An FIA is appropriate for someone who is closer to retirement, prefers tax deferral, principal protection, and market participation. While FIAs may not be appropriate for younger individuals with higher risk tolerance or if they need access to their funds immediately. By allocating 20% of a 60/40 portfolio to an FIA, the portfolio’s risk premium decreases due to the guaranteed protection from the annuity.

What Did We Learn This Week? (03/17/2023) - STILL

Whenever you hear someone talking about the economy and they use the word “still”, your ears should perk up

WealthVest Adds Tanner Isaacson to its Wholesaling Team

WealthVest, a financial services marketing and wholesaling firm, announced that Tanner Isaacson, a well-regarded financial planning professional, has joined their nationwide team as a Regional Consultant.

What Did We Learn This Week? (03/07/2023) - The Godot Recession

Why hasn’t the “most anticipated recession in history” started yet?

WealthVest Expands Distribution Team to Include New National Sales Manager

WealthVest, a leading independent distributor of annuities and structured note solutions to financial institutions, announced today they have named Matt Hamann, a senior veteran in the industry, as their first, dedicated national sales manager representing Aspida, a tech-leading and agile annuity company.

WealthVest Employees Raise $4,000 to Support Homeless Youth

WealthVest’s employees took turns plunging into the frigid waters of the Bozeman Pond as part of a company-wide challenge to raise funds for the Bozeman School District’s McKinney-Vento Homeless Education Program.

Rethinking 60/40 Part 3: How Multi-Year Guaranteed Annuities Can Help

WealthVest believes that there is a natural fit for MYGAs within optimized portfolios. A multi-year guaranteed annuity, or MYGA, is a type of fixed annuity that offers a guaranteed fixed interest rate for a certain period, usually from three to ten years. A MYGA is appropriate for someone who is closer to retirement and prefers tax deferral and a guarantee of investment return. By allocating 20% of a 60/40 portfolio to a MYGA, the portfolio’s risk premium decreases thanks to the guaranteed protection from the annuity.

What Did We Learn This Week? (02/23/2023) - Where are the Workers

What does a new working paper from the NBER and Washington University tell us about quiet quitting and today’s labor environment?

Rethinking 60/40 Part 2: What can we learn about the years when stocks and bonds are both negative?

Rethinking 60/40: What can we learn about the years when stocks and bonds are both negative?

In our last blog post, I discussed the underlying reasons for today’s underperformance of 60/40 portfolios, but let’s look at how much of an anomaly today’s times are and where 2022 falls in history. Since 1928, we can glean the underlying reasons a 60/40 portfolio allocation became popular method for investors seeking reliable returns. The chart below shows historical corporate bond yield and the S&P 500® returns by year, demonstrating how often bonds and stocks remained positive. However, looking at the years in which equities and bonds are negative provides important context for the contemporary market environment.

WealthVest: The Weekly Bull & Bear - Interview with Torsten Slok

In this episode Drew and Tim interview Torsten Slok, Partner and Chief Economist at Apollo. They discuss what a nolanding economic scenario would look like, employment numbers, the struggle to get inflation down to 2%, the housing market and how demographics will affect future growth prospects.

Rethinking 60/40: Part 1-Why investors use 60/40 allocations?

Rethinking 60/40: Why have individuals used 60/40 Allocations for their Retirement Savings?

A portfolio invested in 60% stocks and 40% bonds, commonly known as a 60/40 portfolio, is where many portfolios start before adjusting to a diversified mix based on time horizon, risk tolerance and savings goals. The 60/40 portfolio mix is a tried and true portfolio allocation because it provides market gains during market rallies and fixed income reliability during economic slowdowns. This portfolio is most suitable when interest rates go down, as equities perform well. When interest rates rise, equity returns typically fall.