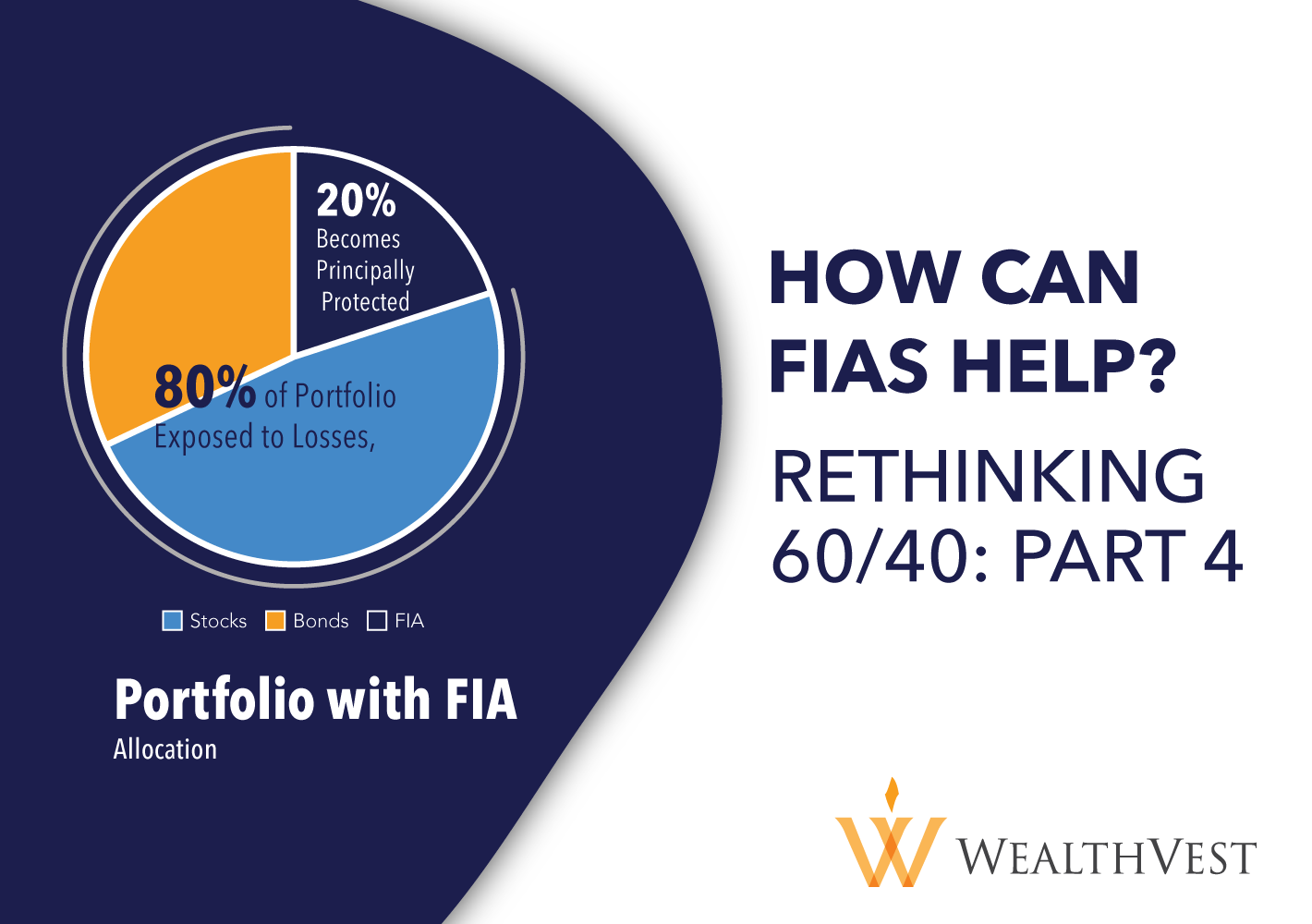

Rethinking 60/40 Part 4: How Fixed Index Annuities Can Help

WealthVest believes that there is a natural fit for FIAs within optimized portfolios A fixed index annuity is a type of fixed annuity that offers a rate of return based on market performance. An FIA is appropriate for someone who is closer to retirement, prefers tax deferral, principal protection, and market participation. While FIAs may not be appropriate for younger individuals with higher risk tolerance or if they need access to their funds immediately. By allocating 20% of a 60/40 portfolio to an FIA, the portfolio’s risk premium decreases due to the guaranteed protection from the annuity.

Rethinking 60/40 Part 3: How Multi-Year Guaranteed Annuities Can Help

WealthVest believes that there is a natural fit for MYGAs within optimized portfolios. A multi-year guaranteed annuity, or MYGA, is a type of fixed annuity that offers a guaranteed fixed interest rate for a certain period, usually from three to ten years. A MYGA is appropriate for someone who is closer to retirement and prefers tax deferral and a guarantee of investment return. By allocating 20% of a 60/40 portfolio to a MYGA, the portfolio’s risk premium decreases thanks to the guaranteed protection from the annuity.

Rethinking 60/40 Part 2: What can we learn about the years when stocks and bonds are both negative?

Rethinking 60/40: What can we learn about the years when stocks and bonds are both negative?

In our last blog post, I discussed the underlying reasons for today’s underperformance of 60/40 portfolios, but let’s look at how much of an anomaly today’s times are and where 2022 falls in history. Since 1928, we can glean the underlying reasons a 60/40 portfolio allocation became popular method for investors seeking reliable returns. The chart below shows historical corporate bond yield and the S&P 500® returns by year, demonstrating how often bonds and stocks remained positive. However, looking at the years in which equities and bonds are negative provides important context for the contemporary market environment.

Rethinking 60/40: Part 1-Why investors use 60/40 allocations?

Rethinking 60/40: Why have individuals used 60/40 Allocations for their Retirement Savings?

A portfolio invested in 60% stocks and 40% bonds, commonly known as a 60/40 portfolio, is where many portfolios start before adjusting to a diversified mix based on time horizon, risk tolerance and savings goals. The 60/40 portfolio mix is a tried and true portfolio allocation because it provides market gains during market rallies and fixed income reliability during economic slowdowns. This portfolio is most suitable when interest rates go down, as equities perform well. When interest rates rise, equity returns typically fall.

Webinar: Tax Efficient Retirement Planning

Join WealthVest's National Sales Manager, Charlie Yoachum, where he will walk through how you can utilize tax season to uncover more of your client's assets, positon tax deferral, and have deeper conversations surrounding retirement savings with your clients.

This webinar will feature WealthVest's 2022 1040 Tax Guide, 2022 Tax Summary, and Taxable Yield Chart. These tools help financial professionals have successful client conversations, and will feature sales ideas you can use in your practice.

WealthVest Publishes Definitive Guide On Retirement Income Planning

WealthVest and Wade Pfau, PH.D., CFA, RICP, release a special edition book, Redefining Retirement: A Safe and Secure Way Down the Mountain. The book features the culmination of Pfau's research on lifetime income and the role of annuities, and a guide on how financial professionals can utilize the concepts from the book with their clients.

HOW IS YOUR BUSINESS IN THE MIDST OF THE PANDEMIC

March 2020 began a vicious market decline that saw portfolio values collapse. On March 23rd the Dow hit a low of 18,213.65*. This was not the first market correction that occurred this century. The first few years of the early 2000’s were marred by the losses of the Dot-com bubble bursting, and fast forward to 2008, we saw the housing bubble burst and the beginning of the “Great Recession.” While, markets have greatly recovered this year, the tumultuous nature of the first few months greatly depleted investors savings.

TODAY’S LONGVEITY PARADOX

The dynamic of life expectancy increasing over one’s lifespan is referred to as the longevity paradox. WealthVest’s newest series, The Longevity Paradox, dives into the risks retirees face. With life expectancy growing over the past century, retirees must plan for an indefinite retirement timeline. Planning for longevity, while balancing investor behavior and market conditions, proves that retirees face an uphill battle when creating a lifetime income plan. Our first paper in the Longevity Paradox series tackles options retires can use to help combat these issues. This is a consumer approved resource that can help guide today’s retirees to options that help mitigate longevity and behavioral risk in retirement.

IS A 9% ANNUAL AVERAGE RETURN ENOUGH FOR YOUR CLIENTS IN RETIREMENT?

How do you demonstrate timing and sequence of returns risk with your clients? The consumer-facing sales tool “The Hatfields and Mccoys” tells a simple yet effective story on sequence of return risk. In the piece, we examine two hypothetical families entering retirement at age 65, but under different circumstances. Both families retire with $500,000 of their nest egg fully invested in the S&P 500® index. They both withdraw 4% annually, with a 2.5% increase each year to keep pace with inflation. The McCoys experience the annual returns from years 1978 to 2008, while the Hatfields experience the same returns, but in reverse chronological order, with a key point being that the annual return for 2008’occurs during their first year of retirement and the return for 1978 is their last.

THE GREATEST BOND BULL MARKET IS OVER…

When I sat down in early February to reevaluate the piece, What’s Your Favorite Fixed Income Alternative, the 10-year treasury hovered near historic lows, by March, they had plunged further than many expected. March was the most volatile month we’ve seen since the Great Depression, not only in equities, but in bonds too. U.S. sovereign debt has traded at highest highs, with yields dropping to .318% on the 10-year and 1.34% on the 30-year*. Falling interest rates have resulted in gains for bond funds and bonds trading in the secondary market. With bonds trading at record highs, talk to your clients about potential bond alternatives for a few reasons.

WHAT IS THE FASTEST GROWING SEGMENT OF THE ANNUITY MARKETPLACE

Have you heard of structured annuities, buffered annuities, registered index-linked annuities or variable index annuities? With so many different names for the same product line it can become confusing but since LIMRA uses registered index-linked annuities (RILAs), I will use it to describe the fastest growing segment in the annuity space and give reasons why sales are accelerating so rapidly.

HOW YOU CAN HELP YOUR CLIENTS IN THIS BEAR MARKET

You are undoubtedly getting phone calls each and every day from your weary and worried clients about what they should be doing with their investments and how today’s events will affect their financial plan. You’ve helped navigate them through the ups and downs of the market in the past, but this is the first time guiding them through a worldwide pandemic. What do you tell them?